Credit Card Delinquency

Credit cards are one of the major ways that consumers hold debt. It can also fluctuate to a greater extent on an individual basis than would be expected from student loans, auto loans, or home mortgages.

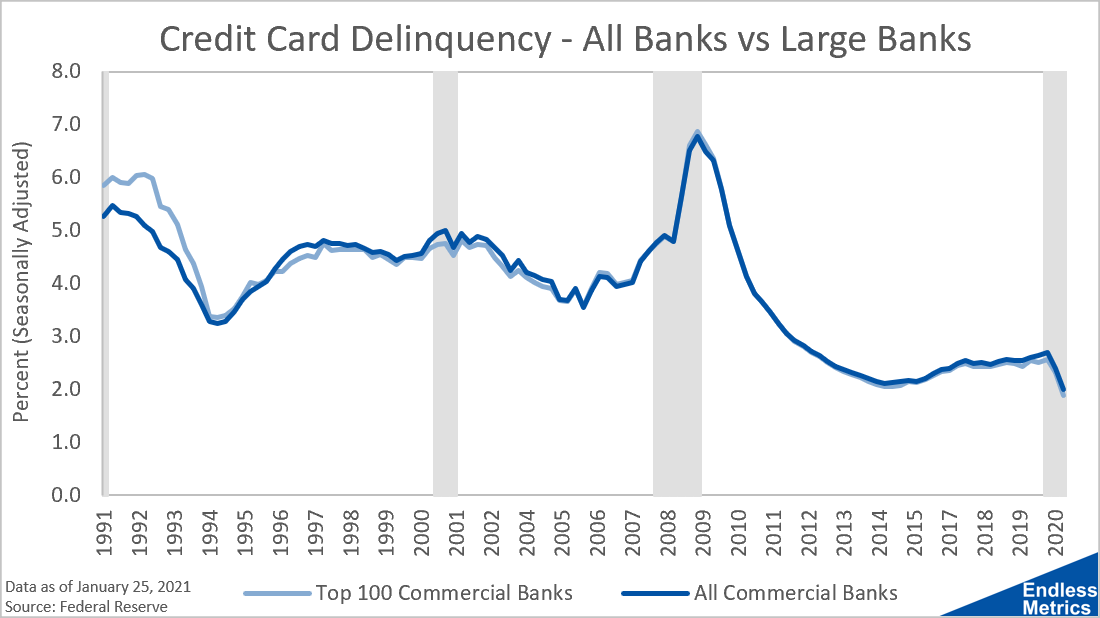

Fortunately, on an aggregated basis, it's behavior isn't particularly volatile and provides a good metric to assess one aspect of debt-burden faced by consumers:

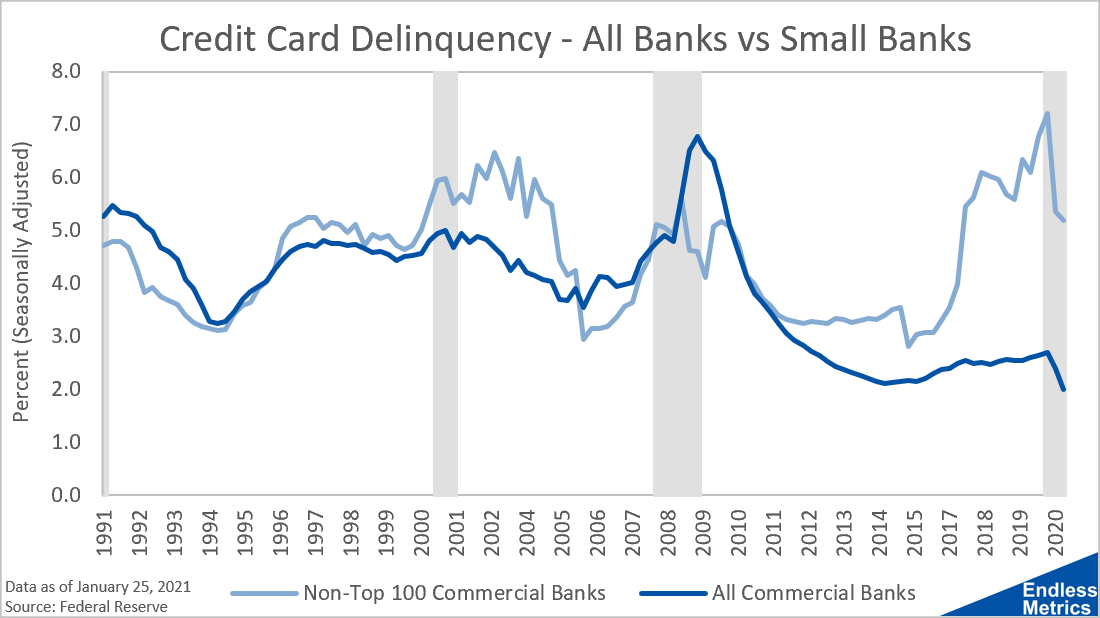

While large banks see delinquency behavior in line with the market (which would be expected as large banks comprise most of the market), smaller banks show a different behavior:

Overall, we can use these indicators to gauge the current and future potential of consumer purchasing ability.

Metrics

S&P 500S&P 500 by Lowest PES&P 500 by Highest PES&P 500 Stock VolumeS&P 500 Stock BetasNasdaq / S&P 500Market CapitalizationHousehold Net WorthNet Worth / GDPReal PCEIndustrial ProductionInitial ClaimsContinuing ClaimsInsured UnemploymentCredit Card DelinquencyBitcoinTED SpreadThe VIXThe Weekly Economic IndexBaa Bond YieldsConsumer CreditThe Unemployment Rate10Y Breakeven Inflation10-2 SpreadReal GDPM2 Money Stock